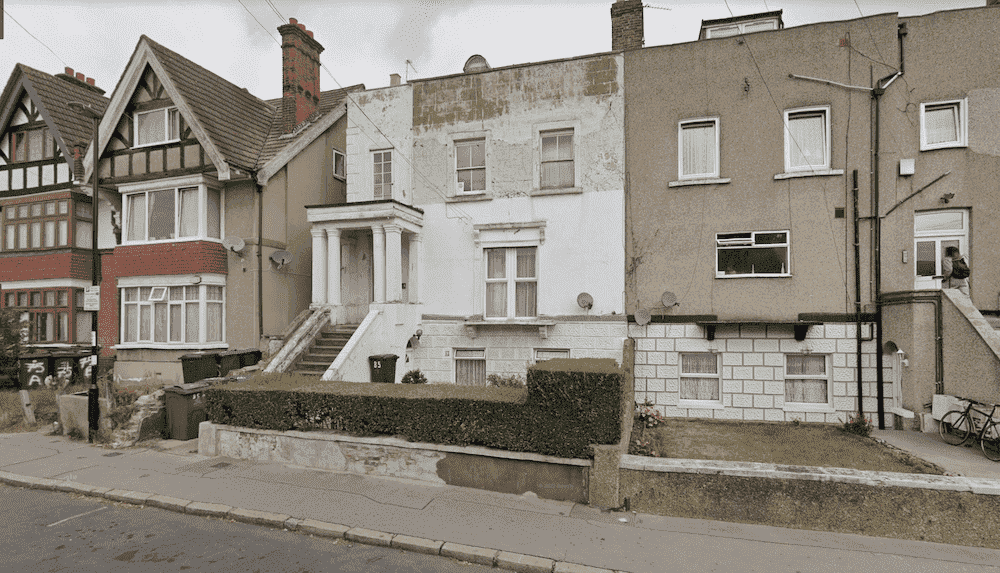

Whetstone London N20 Ground rent investment with one short lease

Greenford Ground Rents for sale with short leases

Total income:

£100

3 flats within a Victorian conversion. None of the units have had their leases extended and there is substantial reversionary value.

Total income:

£150

FREEHOLD GROUND RENT INVESTMENT - 22 FLATS - 9 LEASES WITH 64 YEARS UNEXPIRED

Total income:

£450

London SE9 3QR Ground rent investment

Total income:

£100